This is the third blog in our Data Engineering for Banks series, where we explore how EU banks can modernize their data foundations to stay compliant, agile, and competitive.

Catch up on the previous parts here:

→ Why EU Banks Need Stronger Data Engineering

→ Data Engineering Starts with a Data Assessment

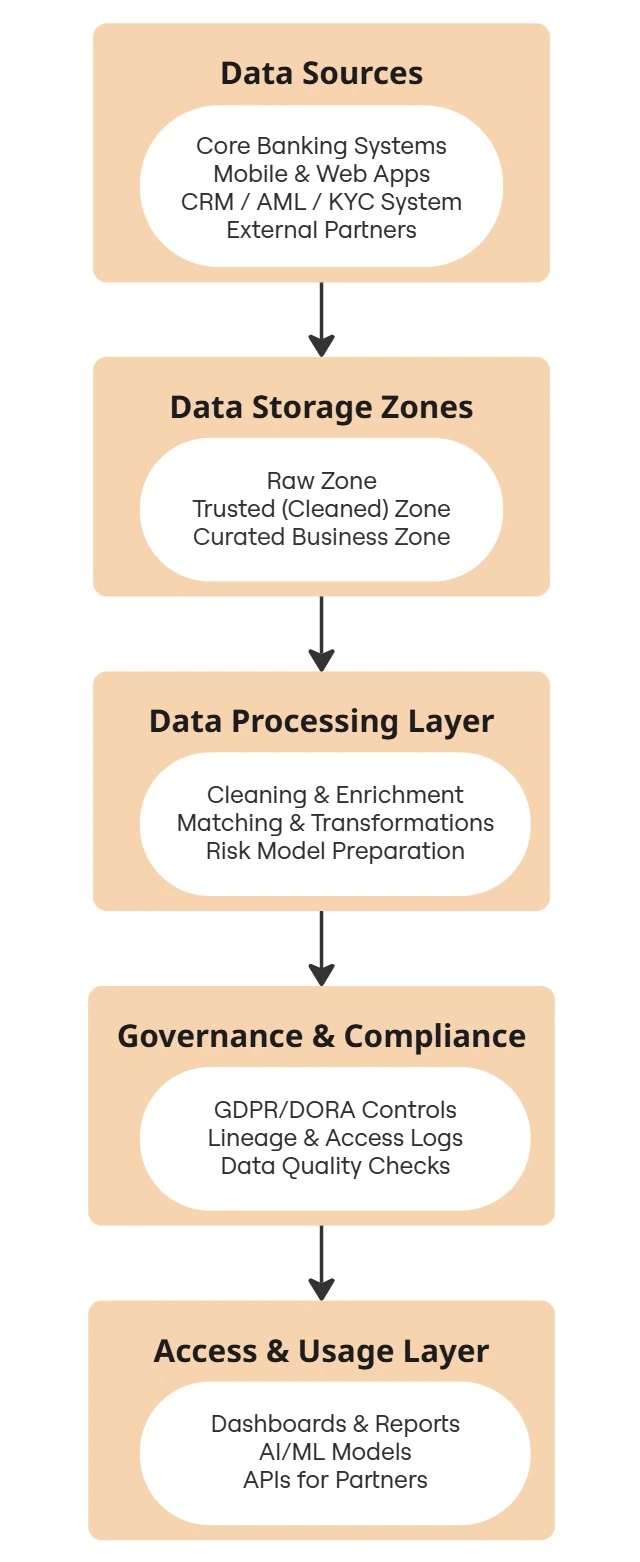

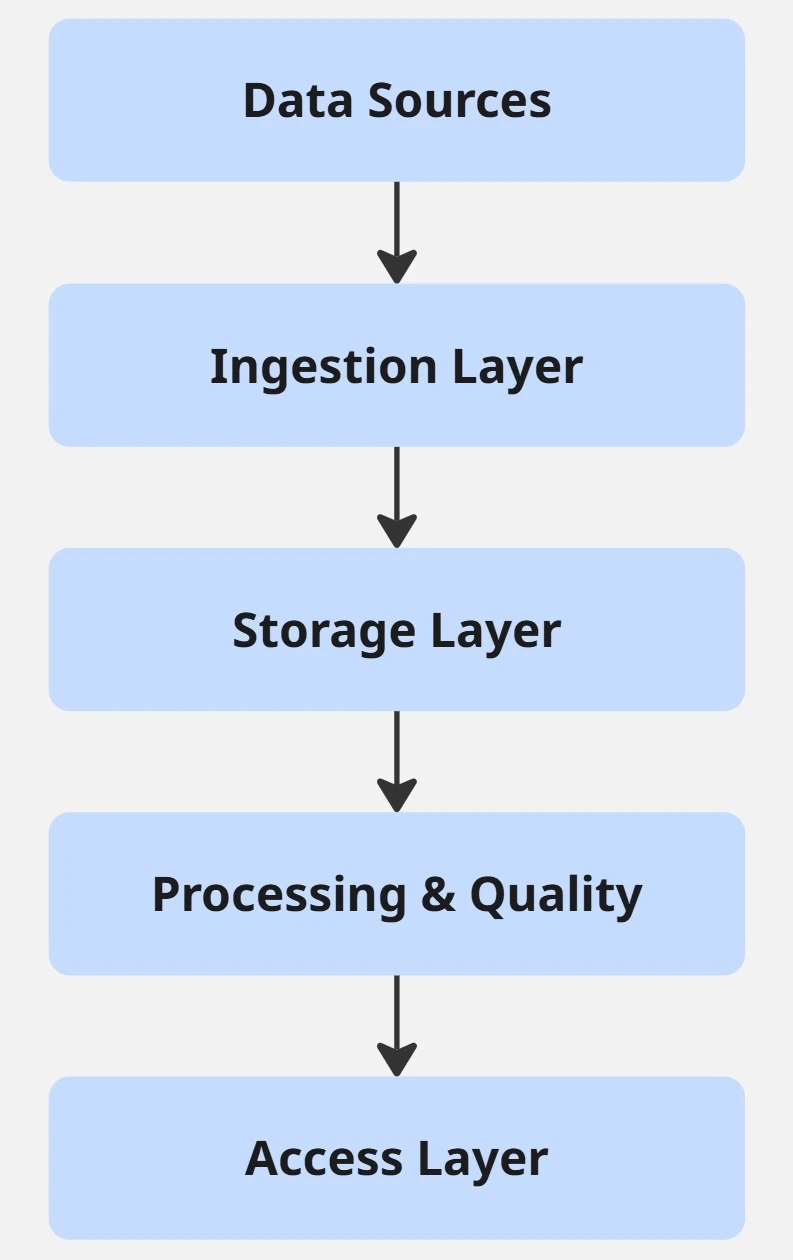

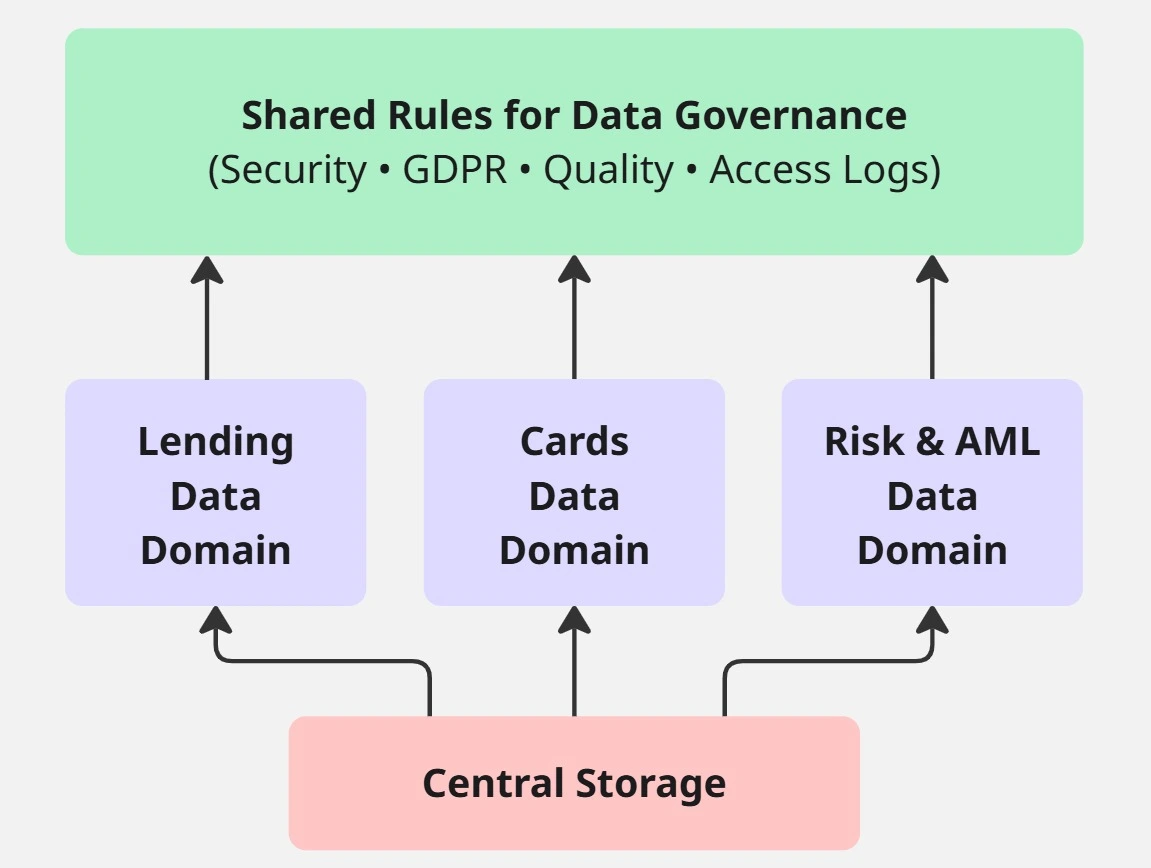

In this part, we’ll focus on how to design a robust data architecture that supports compliance, scale, and smart decision-making for European banks.

18 mins

18 mins

Talk to Our

Consultants

Talk to Our

Consultants Chat with

Our Experts

Chat with

Our Experts Write us

an Email

Write us

an Email